32 housing markets where tight inventory still favors sellers

Want more housing market stories from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter.

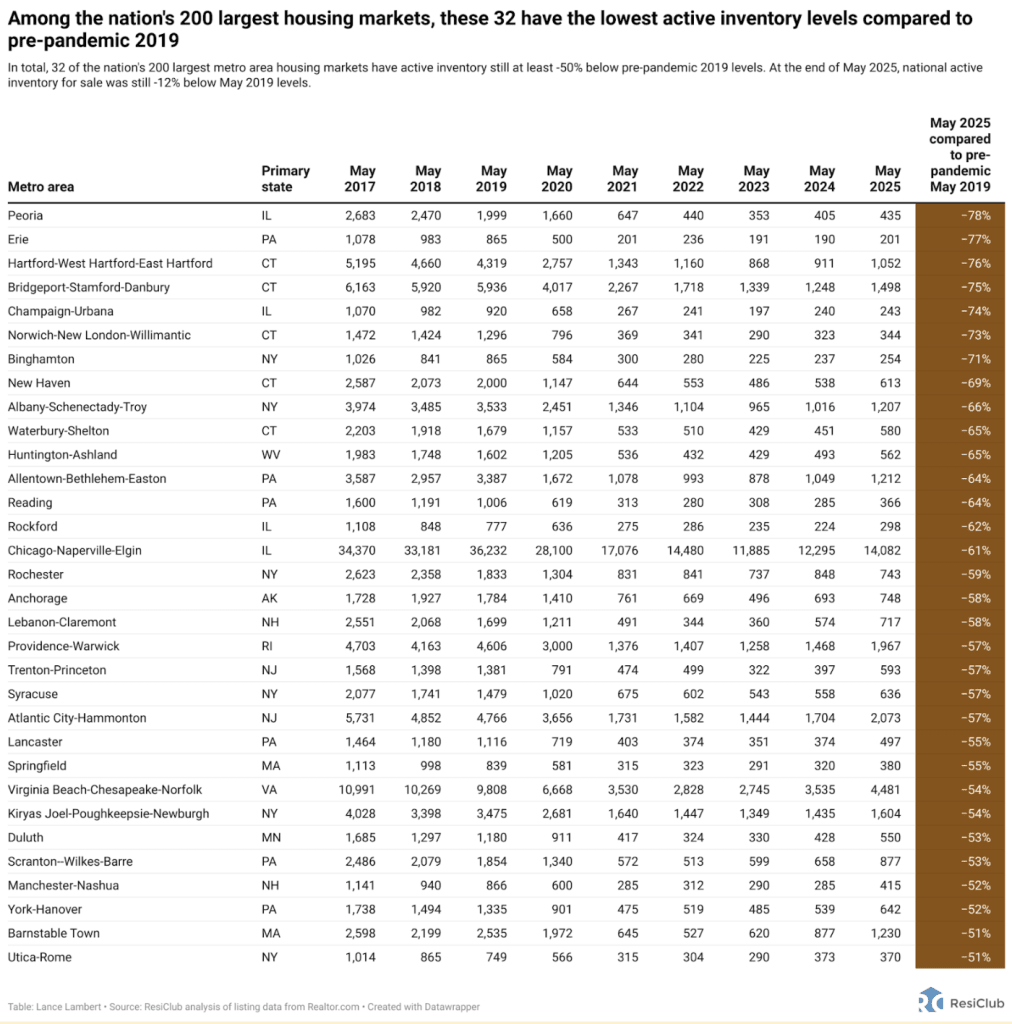

National active housing inventory for sale at the end of May 2025 was up 32% compared to May 2024. That’s just 12% below pre-pandemic levels in May 2019. However, while the national housing market has softened and inventory has surpassed 2019 pre-pandemic levels in some pockets of the Sun Belt, many housing markets remain far tighter than the national average.

Pulling from ResiClub’s monthly inventory tracker, we identified the tightest major housing markets heading into the spring 2025 season, where active inventory is still the furthest below pre-pandemic 2019 levels. These markets are where home sellers have maintained more power compared to most sellers nationwide.

Among the nation’s 200 largest metro area housing markets, 32 markets (see table below) at the end of May 2025 still had at least 50% less active inventory than in May 2019.

That’s lower than last month’s count, when 37 of the nation’s 200 largest metro area housing markets still had active inventory at least 50% below pre-pandemic 2019 levels—and down from 42 of the 200 the month before that.

Many of those tight markets are in the Northeast, in particular, in states like New Jersey and Connecticut.

Unlike the Sun Belt, many markets in the Northeast and Midwest were less reliant on pandemic-era migration and have fewer new home construction projects in progress. With lower exposure to the negative demand shock caused by the slowdown in pandemic-era migration—and fewer homebuilders in these regions offering affordability adjustments once rates spiked—active inventory in many Northeast and Midwest housing markets has remained relatively tight, maintaining a seller’s advantage heading into spring 2025.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0