Housing market shift: Where homebuyers are taking power fast

Want more housing market stories from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter.

When assessing home price momentum, ResiClub believes it’s important to monitor active listings and months of supply. If active listings start to rapidly increase as homes remain on the market for longer periods, it may indicate pricing softness or weakness. Conversely, a rapid decline in active listings could suggest a market that is heating up.

Since the national Pandemic Housing Boom fizzled out in 2022, the national power dynamic has slowly been shifting from sellers to buyers. Of course, across the country that shift has varied significantly.

Generally speaking, local housing markets where active inventory has jumped above pre-pandemic 2019 levels have experienced softer home price growth (or outright price declines) over the past 36 months. Conversely, local housing markets where active inventory remains far below pre-pandemic 2019 levels have, generally speaking, experienced more resilient home price growth over the past 36 months.

Where is national active inventory headed?

National active listings are on the rise (+25% between July 2024 and July 2025). This indicates that homebuyers have gained some leverage in many parts of the country over the past year. Some sellers markets have turned into balanced markets, and more balanced markets have turned into buyers markets.

Nationally, we’re still below pre-pandemic 2019 inventory levels (-11% below July 2019) and some resale markets, in particular, big chunks of Midwest and Northeast, still remain tight-ish.

While national active inventory is still up year-over-year, the pace of growth has slowed in recent weeks—more than typical seasonality would suggest—as some sellers have thrown in the towel and delisted (more on that in another piece).

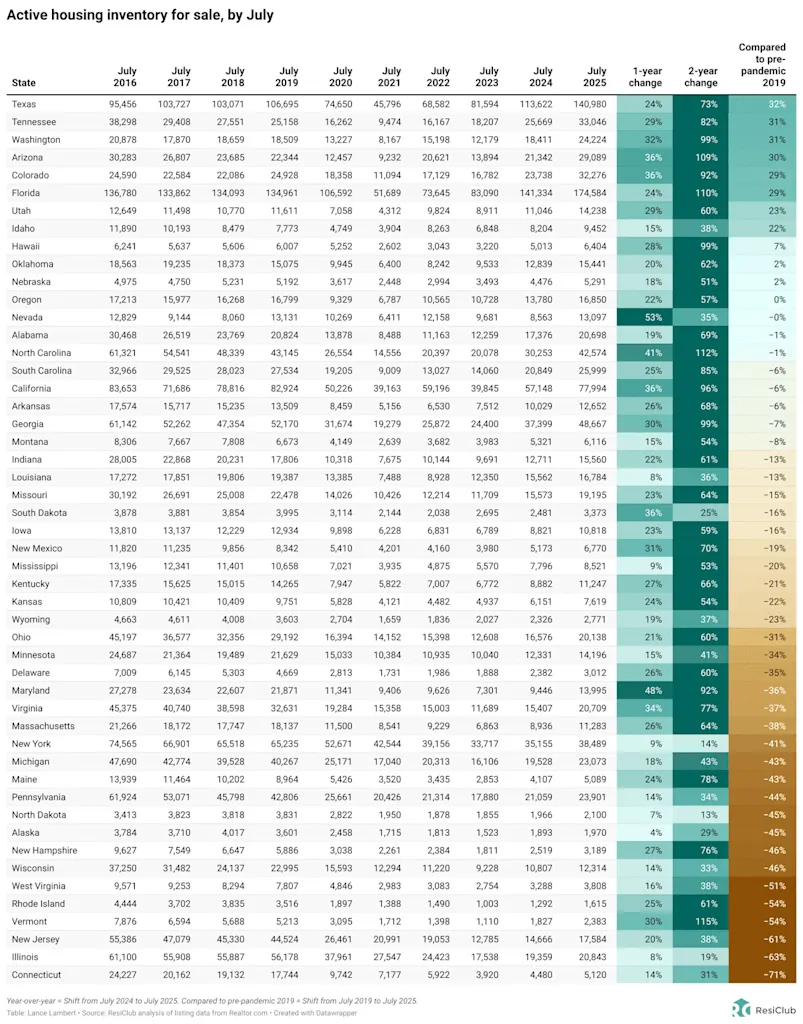

July inventory/active listings* total, according to Realtor.com:

- July 2017 -> 1,322,659 📉

- July 2018 -> 1,261,916 📉

- July 2019 -> 1,239,534 📈

- July 2020 -> 822,834 📉

- July 2021 -> 546,686 📉

- July 2022 -> 691,652 📈

- July 2023 -> 647,135 📈

- July 2024 -> 884,273 📈

- July 2025 -> 1,102,787 📈

IF we maintain the current year-over-year pace of inventory growth (+218,514 homes for sale), we’d have:

- 1,321,301 active inventory come July 2026

- 1,539,815 active inventory come July 2027

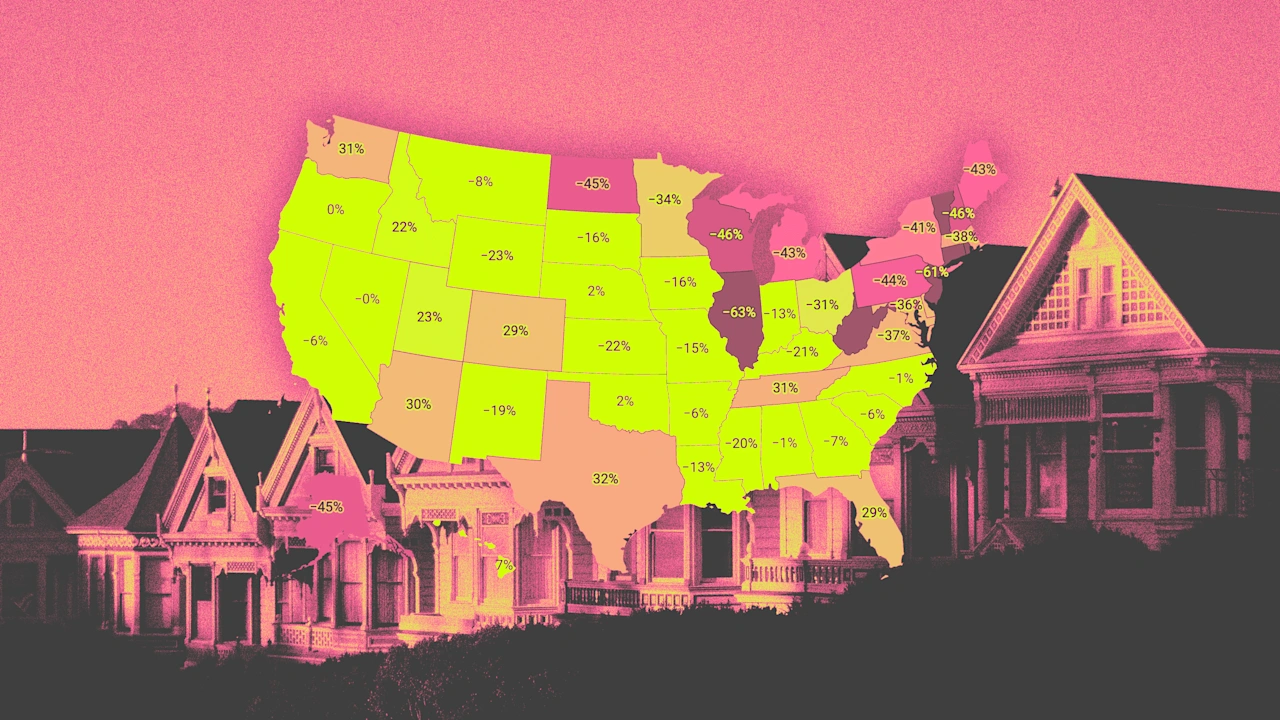

Below is the year-over-year percentage change by state.

While active housing inventory is rising in most markets on a year-over-year basis, some markets still remain tight-ish (although it’s loosening in those places too).

As ResiClub has been documenting, both active resale and new homes for sale remain the most limited across huge swaths of the Midwest and Northeast. That’s where home sellers this spring had, relatively speaking, more power.

In contrast, active housing inventory for sale has neared or surpassed pre-pandemic 2019 levels in many parts of the Sun Belt and Mountain West, including metro area housing markets such as Punta Gorda and Austin. Many of these areas saw major price surges during the Pandemic Housing Boom, with home prices getting stretched compared to local incomes. As pandemic-driven domestic migration slowed and mortgage rates rose, markets like Tampa and Austin faced challenges, relying on local income levels to support frothy home prices.

This softening trend was accelerated further by an abundance of new home supply in the Sun Belt. Builders are often willing to lower prices or offer affordability incentives (if they have the margins to do so) to maintain sales in a shifted market, which also has a cooling effect on the resale market: Some buyers, who would have previously considered existing homes, are now opting for new homes with more favorable deals. That puts additional upward pressure on resale inventory.

In recent months, that softening has accelerated again in West Coast markets too—including much of California.

At the end of July 2025, 12 states were above pre-pandemic 2019 active inventory levels: Arizona, Colorado, Florida, Idaho, Hawaii, Nebraska, Oklahoma, Oregon, Tennessee, Texas, Utah, and Washington. (The District of Columbia—which we left out of this analysis—is also back above pre-pandemic 2019 active inventory levels too. Weakness in D.C. proper predates the current admin’s job cuts.)

Big picture: Over the past few years we’ve observed a softening across many housing markets as strained affordability tempers the fervor of a market that was unsustainably hot during the Pandemic Housing Boom. While home prices are falling in many pockets of the Sun Belt, a big chunk of Northeast and Midwest markets saw a little price appreciation this spring. That said, given the current softening, ResiClub still expects that as the year progresses, more markets will fall into the year-over-year decline camp.

Below is another version of the table above—but this one includes every month since January 2017.

If you’d like to further examine the monthly state inventory figures, use the interactive below. (To better understand ongoing softness and weakness across Florida, read this ResiClub PRO report.)

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0